Pa Public Pensions Mamagemant and Asset Review Commission

State Pension Funds Reduce Assumed Rates of Return

Projections of lower economic growth fueling a 'new normal' in expected investment performance

The cursory was revised on Jan. 13, 2020 to remove an outdated render forecast.

Overview

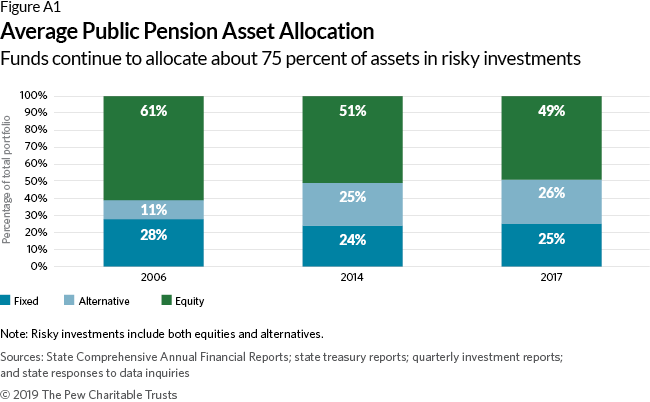

Country and local public employee retirement systems in the United states manage over $4.3 trillion in public pension fund investments, with returns on these assets bookkeeping for more than sixty cents of every dollar available to pay promised benefits. Nigh three-quarters of these avails are held in what are oftentimes chosen risky assets—stocks and alternative investments, including private equities, hedge funds, real estate, and bolt.1 These investments offer potentially higher long-term returns, but their values fluctuate with ups and downs in financial markets in the short term and the broader economy over the long run.

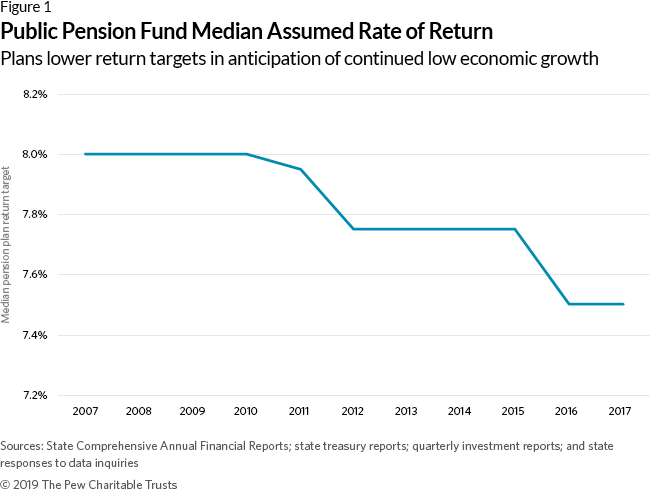

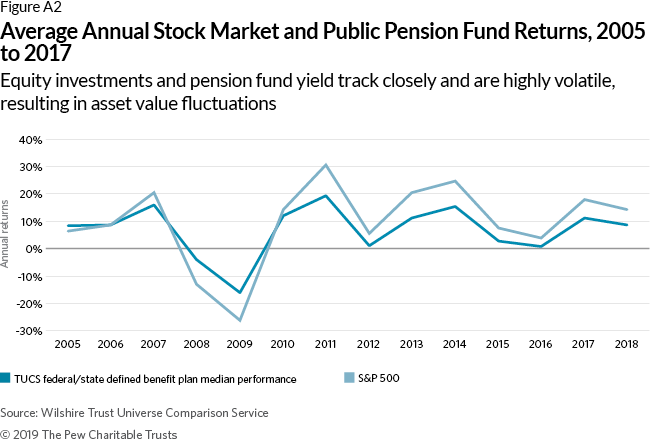

Fiscal analysts now expect public pension fund returns over the adjacent two decades to be more than than a full pct betoken lower than those of the by, based on forecasts for lower-than-historical involvement rates and economic growth. Research by The Pew Charitable Trusts shows that since the Great Recession—which started in late 2007 and officially concluded in mid-2009—public pension plans have lowered return targets in response to changes in the long-term outlook for financial markets. (Meet Effigy 1.)

Pew'south database includes the 73 largest state-sponsored alimony funds, which collectively manage 95 percent of all investments for land retirement systems. The average assumed return for these funds was vii.three percent in 2017, down from over 7.v percent in 2016 and viii per centum in 2007 but earlier the downturn began.

More than half of the funds in Pew's database lowered their causeless rates of render in 2017. Following the steep swings during the recession and in the years immediately afterward, these changes reverberate a new normal in which forrard-looking projections of expected economic growth and yields on bonds are lower than those that state pension funds have historically enjoyed. Reducing the causeless rate of return leads to increases in reported programme liabilities on fund balance sheets, which in turn increases the actuarially required employer contributions. Still, making such changes tin can ultimately strengthen plans' fiscal sustainability by reducing the adventure of earnings shortfalls, and thus limiting unexpected costs.

Recently, many plans have worked to mitigate the higher required contributions that have been prompted by increased liabilities linked to more than conservative investment assumptions. The present value of future liabilities is typically calculated using the assumed rate of render equally the discount rate, which is used to limited future liabilities in today's dollars; lower return assumptions yield college calculated liabilities. Some country alimony funds accept phased in discount rate reductions—effectively altering how they compute future liabilities. That allows them to spread out increases in contributions over time.

For example, in 2016, the California Public Employees Retirement System (CalPERS)—the nation'southward largest public alimony plan—announced it would decrease its assumed rate of return incrementally from 7.5 percent in 2017 to 7 pct by 2021.2 Fifty-fifty such an incremental change tin accept a significant bear on over fourth dimension: a 1 per centum point driblet in the discount charge per unit would increase reported liabilities across U.S. plans by over $500 billion, a 12 per centum ascent.

As assumed returns have gone down, asset mixes have remained largely unchanged. For example, average allocations to stocks and alternative investments—which can provide higher yields but with greater adventure, complication, and cost—have remained relatively stable in contempo years at around 50 pct and 25 percent of assets, respectively. This indicates that most fund managers and policymakers are adjusting their assumed rates of return in response to external economic and market forecasts, not based on shifts in internal investment policies.

This cursory updates research published by Pew in 2017 and 2018 that provided information on asset allocation, functioning, and reporting practices for funds in all l states. It explores the impact of connected slow economic growth on investment performance, likewise as potential management and policy responses to lower returns. Finally, the brief highlights policies and solutions employed by well-funded plans, including the adoption of lower render assumptions, that have helped insulate the plans from economical volatility.

Key Terms and Concepts

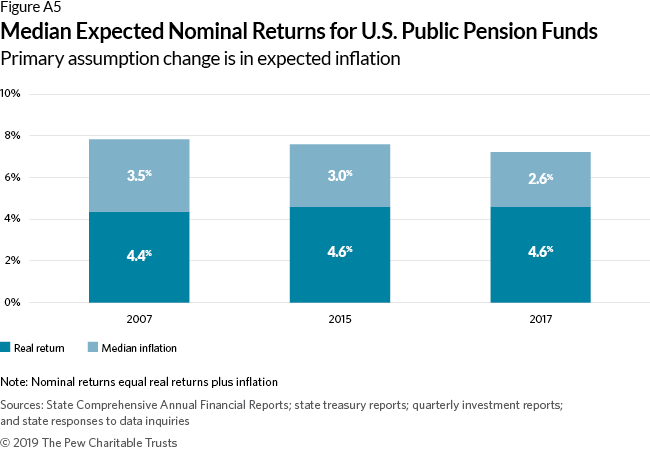

Causeless charge per unit of return: The causeless, or expected, rate of return is the return target that a pension fund estimates its investments will deliver based on forecasts of economic growth, inflation, and involvement rates. The median state pension fund had an assumed rate of return of 7.42 percentage in 2017 and the average was seven.33 percent.

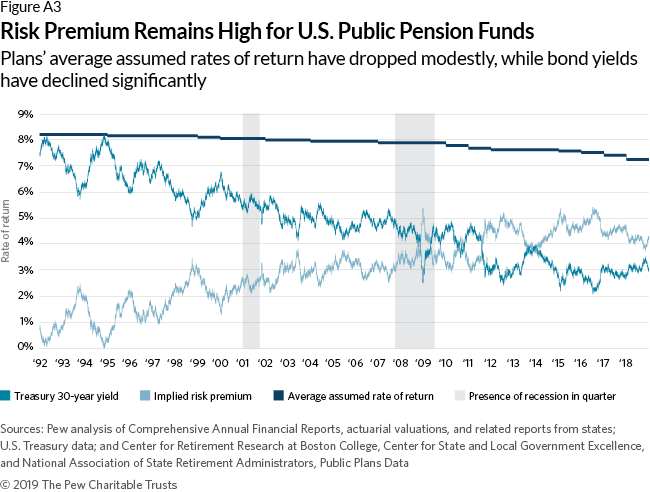

Disbelieve rate: The discount rate is used to express time to come pension liabilities in today's dollars. Most land pension funds determine their discount rate based on their assumed charge per unit of render. Decreasing a plan's discount rate leads to higher calculated liabilities, and higher required almanac contribution payments. The median country pension fund had a discount charge per unit of 7.25 percent in 2017 and the boilerplate was vii.11 percent.

Investment fees: Investment fees or expenses include any fees that a pension fund pays to professionals to classify its assets. These can be administrative or money management fees, and would include any payments for performance or profit-sharing arrangements, if reported.

Real and nominal returns: The real return is the return an investor receives after the rate of inflation is subtracted from the nominal rate (real return = nominal return – aggrandizement).

Risky assets: The Federal Reserve defines "safe assets" as fixed-income investments, cash, and other cash equivalents (e.g., certificates of deposit). Risky avails include other investments, such equally equities (stocks), private equities, hedge funds, real manor, and commodities that are expected to generate college returns but expose funds to greater marketplace volatility.

State alimony fund and state pension plan: States frequently sponsor more than one pension plan for participating workers and retirees; individual plans inside a country are usually divided by the employing government bureau. Plans are tasked with administering pension benefits, while state pension funds manage the investment of program assets.

Slow economic growth projected for the side by side decade

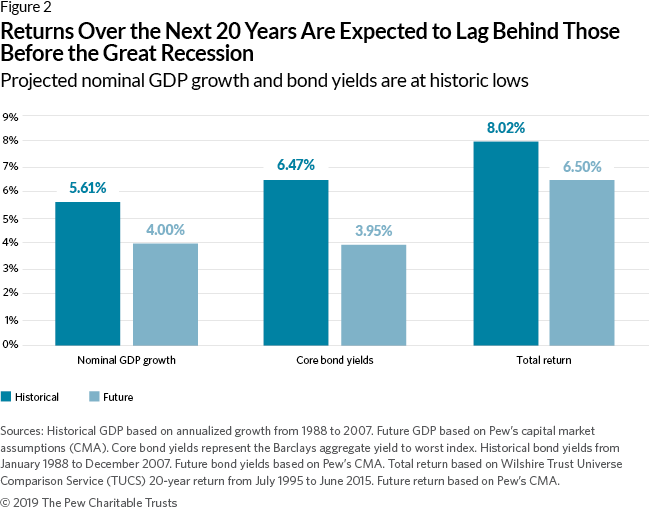

Forecasts of lower-than-historical economic growth and bond yields over the side by side 10 to 20 years drive the growing consensus amongst authorities and industry economists that pension funds will see lower long-term investment returns and propose a new normal for public fund investments. For example, the U.South. experienced annual gross domestic product (Gdp) growth of more than 5.5 percent from 1988 through 2007, while the Congressional Budget Office (CBO) now projects only 4 percentage annual growth for the side by side decade. (Run across Figure 2.) And as economical growth is expected to perform more modestly, the long-term outlook for stocks and other investments that pension funds hold will be similar.

Returns on bonds, which make up nigh 25 percent of pension fund assets, are likewise projected to be lower than historical averages. Investment-grade bond yields between 1988 and 2007 averaged most 6.5 percentage a year, only the CBO projects an boilerplate of just 3.7 percent annually through the side by side decade.three

Given these trends, marketplace experts generally concur that lower investment returns will persist going forward. Pew forecasts a long-term median return of only 6.4 percent a yr for a typical pension fund portfolio, considering expected Gross domestic product growth and interest rates.4 Other analysts with like projections include Voya Fiscal Advisors (6.iv percentage), J.P. Morgan and Wilshire (both 6.five pct).5

Key trend: Lower assumed returns

Investment returns make upwards more than 60 percent of public pension plan revenues—employer and employee contributions brand upwardly the rest—so funds need accurate return assumptions to ensure fiscal sustainability. A decade into the recovery, states accept an opportunity to recalibrate policies to the economy'south "new normal" by adopting return assumptions in line with current projections.

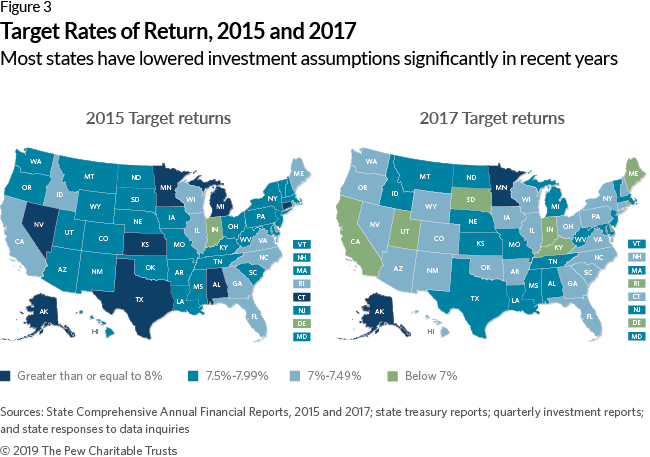

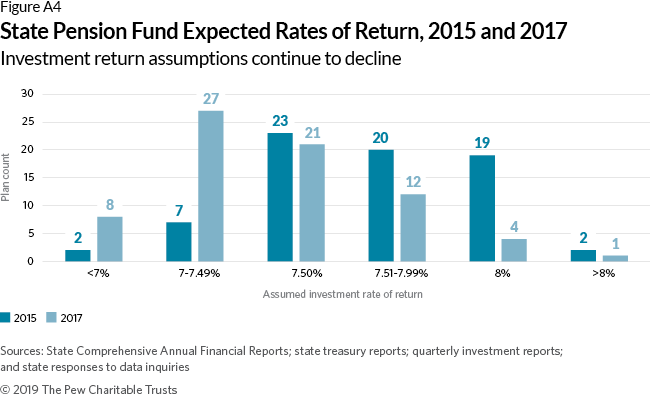

Many plans take lowered their causeless rates of render—which also affects discount rates—to reflect these economic realities, despite the virtually-term budget challenges they may confront as contribution requirements rise with lower discount rates. For case, while simply nine of the 73 funds in this written report had an assumed rate beneath 7.5 percentage in 2014, by the stop of financial year 2017, about half had adopted assumed rates beneath that percentage. 40-two of the funds reduced their causeless rate in 2017 to better account for lower expected investment returns. Several states—including Georgia, Louisiana, Michigan, and New Jersey—take followed the case of California's CalPERS fund by adopting multiyear strategies to ramp downwards assumed rates over the next several years.

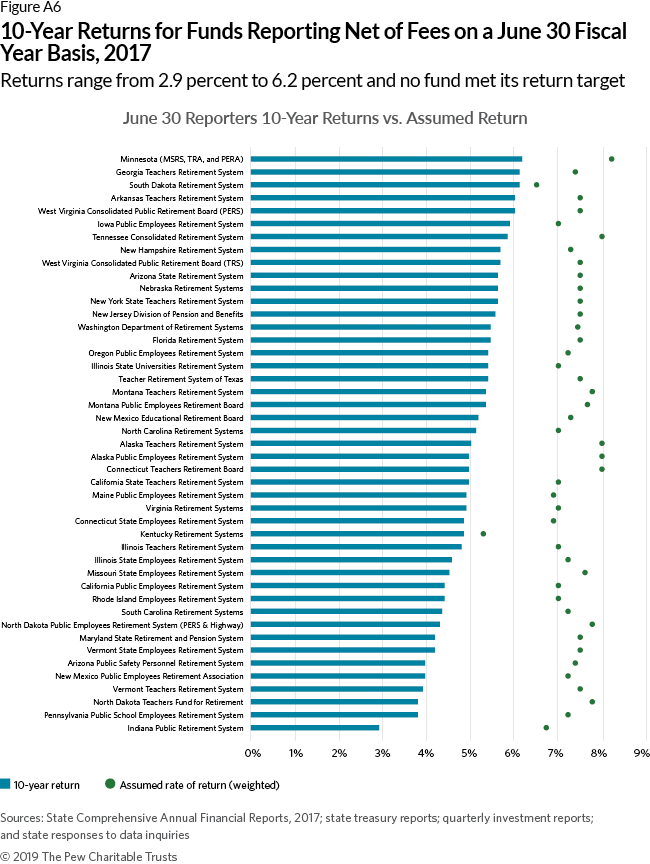

Policymakers may raise concerns about the rise in the present value of pension fund liabilities caused past lowering discount rates, the resulting reduction in funded ratios (the share of a plan's liabilities matched by assets), and the bear upon of these changes on required contributions for employers and workers. However, the impact on liabilities reflects accounting, non economic science. Ultimately policymakers need to construction retirement systems to ensure financial sustainability throughout the economic wheel so members receive promised benefits. Although pension funds enjoyed robust investment returns in 2017 (the median one-yr return across the 73 funds was 12.8 percent), funds continue to underperform relative to their long-term return targets. For example, in 2017 the median return over the prior 10 years was less than 5.five percent, and none of the funds in our information met their investment target over that catamenia.

States acting to adopt more bourgeois assumptions

States are addressing these concerns. Recent reforms in Connecticut provide an example of how a reduction in discount rates can help mitigate long-term risks and avoid short-term spikes in contribution requirements. The state reduced the disbelieve rates for the Connecticut State Employees' Retirement System (SERS) and Teachers' Retirement Organisation (TRS) from 8 per centum to 6.9 percent in 2017 and 2019 respectively. Concurrently, policymakers adopted a funding policy that would bring downwardly the unfunded liability and stabilize long-term contribution rates.vi Finally, they extended the fourth dimension period for the state to pay down the more than $30 billion in pension debt to thirty years and added a 5-year phase-in of the new funding policies. Collectively, these policies helped ensure that the bear upon of increased employer contributions would only gradually bear upon the state upkeep.

As expected, Connecticut'due south changes resulted in an increment in the country'south reported alimony debt—the recent reduction in the discount rate for the TRS raised the reported unfunded liability for that system solitary from $xiii billion to virtually $17 billion. But the changes ultimately set the state on a path to pay downwards that debt in a sustainable way that increases the state's cost predictability and insulates the pension funds from marketplace volatility. Indeed, rating agency analyses of Connecticut's credit have taken a forward-looking approach that considers future market gamble and long-term financial sustainability next with the reported funding ratio.

For instance, Fitch Ratings, in its analysis of Connecticut'southward 2019 TRS reform proposal, noted that the fund's previous assumed almanac render of 8 percent was an "unrealistic target for future investment returns ... resulting in actuarial contributions that are inadequate to support long-term funding comeback, thus exposing the land to severe fiscal take chances." The rating agency noted the alter to an expected return of vi.9 percentage as a factor that would lower fiscal risks.7

Other states accept adopted alternative approaches to increase cost predictability and create a margin of prophylactic against inevitable market downturns. In California, CalPERS put in place a take a chance policy in 2015 that incrementally reduces the program's assumed rate of return and shifts its investment mix to less risky avails each twelvemonth that funded levels increase because of better-than-expected returns. Such policies help gradually reduce gamble and increment cost predictability over the long term in a style that doesn't put short-term pressure level on the state budget.8

The Wisconsin Retirement System (WRS) takes an innovative approach to managing risk through render assumptions. The WRS' long-term render assumption for 2017 was 7.2 percent; notwithstanding, the plan uses a lower discount charge per unit of 5 per centum to summate the cost of benefits for workers once they retire.9 Even if investments autumn short of the long-term return assumption, the amount set aside for each retiree should be enough to pay for the base of operations benefit without additional contributions from taxpayers or electric current employees. And, if the returns exceed 5 percent, as they at present are expected to do, the backlog will be used to fund an annuity increment (similar to a cost of living adjustment). The system would not provide such a heave when returns fall below 5 percent.10

Finally, N Carolina effectively uses two discount rates to set contribution policy. The land determines a contribution floor based on the programme's investment render supposition of 7 percent, also as a ceiling using yields on U.S. Treasury bonds as a proxy for what a risk-complimentary investment could return.11 That risk-free rate reflects what a guaranteed investment could deliver; state pension plans, similar nigh other investors, accept on adventure to earn yields in a higher place that charge per unit. If the programme is fully funded under the risk-costless rate, then employer contributions would drop to only pay for the price of new benefits. Any year in which the contribution rate is betwixt the floor and the ceiling, employers will put in an boosted .35 percent of pay above the prior yr'south rate.

The policies put in place by CalPERS, Wisconsin, and Northward Carolina are designed to improve ensure that adequate avails are set up aside to pay for promised benefits, given the cardinal uncertainty of relying on risky investments over a decades-long time horizon. In addition, past lowering their assumed rates of return, more than than half of state pension funds made information technology more likely that they'll exist able to hit their investment targets in future years.

As well as adjusting render targets to reflect irresolute economic conditions, funds are looking more closely at the fees they pay investment managers. According to the Institutional Limited Partners Clan (ILPA), over 140 institutions—including many state and local pension funds—take moved to increment disclosure and transparency for individual equity performance fees (also known as carried involvement).12 These fees business relationship for approximately $half-dozen billion, or thirty per centum of all fees U.Southward. state and local funds reported paying to investment managers in 2017 (direction fees make upwards the balance). For state pension funds to accurately report their operation fees, private equity managers demand to disclose the total price tag to their clients; an expectation that these fees would be disclosed simply recently emerged across state pension funds.

Although fee levels in aggregate have remained relatively constant as a percentage of avails over the terminal decade or more, some funds take managed meaning reductions. For example, in Pennsylvania, reported investment expenses equally a percent of assets accept declined from 0.81 per centum in 2015 to 0.74 percentage in 2017, a shift that saves state alimony plans more $57 one thousand thousand annually in reduced fees. The state continues to focus on the consequence, following the recommendations of its public pension management and asset investment review committee.13 Lawmakers put the panel in place as part of the 2017 state pension reforms, and it has recommended deportment projected to offer actuarial savings betwixt $viii billion and $10 billion over 30 years.

What factors drive projections of lower-than-historical market place returns?

During the bull markets of the 1980s and 1990s, managers of state and local pension funds commonly causeless that over the long term they would earn an average of viii percentage returns, or college, on their investments—assumptions that were, for the most part, fair given the prevailing marketplace outlook of that fourth dimension. All the same, years into the post-recession recovery of today, market place experts project lower returns, in large part because of lower-than-historical economical growth and interest rates.

Economic growth is virtually commonly measured through changes in Gross domestic product, the aggregate level of goods and services produced in a national economic system over a specific fourth dimension period. That measure of growth, in turn, is reflected in market returns for stocks and the value of equity investments. Two key factors that spur growth are the size of the workforce and technology-driven increases in productivity (i.e., the output per worker).

Gdp growth since the Bang-up Recession is lower than growth rates experienced during previous recoveries likewise equally long-term historical averages, in large part because reduced labor force participation has persisted throughout the recovery, despite an unemployment rate that has fallen to its lowest betoken since the 1960s (i.due east., fewer people are in the job market at present than in the past).14 Labor force participation is expected to decline further, and remain beneath historical levels, primarily because the population is crumbling. And productivity increases, the other key driver of Gdp growth, are expected to be small, absent unforeseen pregnant technological innovations.fifteen

At the same time, the corporeality of interest that government and corporate bonds pay has steadily declined over the past 30 years. Afterwards the recession, the U.S. entered an unprecedented period of low interest rates, with the Federal Reserve keeping short-term rates at or near cypher from 2008 to the terminate of 2015. Yields on the 30-twelvemonth Treasury annotation fell from 8 per centum in 1990 to about 3 percent at the end of 2018, and recently have dropped even further.

Looking alee, most experts do non look a significant rise in interest rates in the well-nigh term for several reasons, prime amongst them that inflation has been low the by five years and is forecast to remain beneath average for the long term.sixteen Factors that typically raise aggrandizement, such as wage increases and economical development, are non expected to amend chop-chop or put significant upward force per unit area on the cost of appurtenances and services.17

Decision

The economy is expected to abound at a pocket-size charge per unit over the adjacent decade, and pension fund investment returns are unlikely to return to celebrated levels for the foreseeable futurity. In recognition of these trends, public plans are increasingly adjusting their render assumptions to rates more in keeping with economic forecasts.

Although reported liabilities will rise considering plans are calculating the cost of pension promises using more than conservative assumptions, the lower assumed rates of return ultimately decrease alimony funds' investment risk, increase pension price predictability for taxpayers, and cistron positively in state credit analyses. By pairing the reductions in the discount rate with policies to smooth out the toll affect or by adopting such changes equally role of broader reform efforts, policymakers tin can moderate the bear on on land and local budgets.

States can adopt policies that provide a margin of safety for pension systems in the likely upshot of an eventual economic downturn. California, North Carolina, and Wisconsin provide examples of alternative approaches that tin reduce investment risk for public pension funds and government budgets akin.

Appendix

To examine investment practices of pension funds across the 50 states, Pew uses iii sources covering the 73 largest land-sponsored alimony funds, which collectively take assets under direction of over $iii trillion (about 95 percent of all state pension fund investments). Twenty-two states have more than one fund:

- Data collected from country-sponsored plans' Comprehensive Annual Fiscal Reports, pension plan investment reports, and other relevant documents published by private public pension plans from 1992 through 2017, with a main focus on asset allocation, functioning, and fees from 2006 to 2017. In add-on, performance data from 2018 were collected from program documents.

- The U.S. Federal Reserve Financial Accounts of the United States data, which include aggregate economic and investment information on public pensions from 1950 through 2018.

- The Wilshire Trust Universe Comparing Service (TUCS) performance comparing data, reported quarterly from 1991 through 2018.18

- Together, these datasets provide more than than lx years of aggregate investment trends and permit for a detailed wait at investment practices from 2006 to 2017 across most state public pension funds. Complete 2017 data— in tabular and graph class—can be institute in the appendix.

Table A1: Public Pension Investment Metrics Across the 50 States, 2017

Come across PDF for full table

Endnotes

- Lath of Governors of the Federal Reserve System, "Z.1 Financial Accounts of the United States: Flow of Funds, Balance Sheets, and Integrated Macroeconomic Accounts, Fourth Quarter 2018," Table L.120, Federal Reserve Statistical Release, March 7, 2019, https://www.federalreserve.gov/releases/z1/20190307/z1.pdf.

- Come across California Public Employees Retirement System, "CalPERS to Lower Discount Rate to Seven Percent Over the Next Iii Years," news release, December 21, 2016, https://www.calpers.ca.gov/page/newsroom/calpers-news/2016/calpers-lower-discount-rate; and Sovereign Wealth Fund Found, "Top 100 Largest Public Pension Rankings past Total Avails," https://world wide web.swfinstitute.org/fund-rankings/public-pension.

- Congressional Budget Function, "The Upkeep and Economical Outlook: 2019 to 2029" (2019), https://www.cbo.gov/system/files/2019-03/54918-Outlook-iii.pdf.

- G. Mennis, Southward. Banta, and D. Draine, "Assessing the Risk of Fiscal Distress for Public Pensions: Country Stress Test Analysis" (Mossavar-Rahmani Middle for Business organisation and Regime Associate Working Paper No. 92, Harvard Kennedy School, 2018).

- Run into P. Zemsky and B. Reinhard, "2019 Majuscule Market place Assumptions" (2018), New York: Voya Investment Direction; and J.P. Morgan Asset Management, "2017 Long-Term Capital Market place Assumptions" (2017), New York: J.P. Morgan Chase & Co.; and A. Foresti and M. Blitz, "2017 Asset Allotment Return and Risk Assumptions" (2017), Santa Monica, California: Wilshire Consulting.

- Actuarial funding policies for pension plans are split between those using level dollar payments for fund pension debt, where the dollar amount going to shut the funding gap is expected to stay stable over fourth dimension, and level percent of payroll funding policies, where the debt payment will stay constant equally a share of total salary simply will grow in dollar terms. The former has a college initial dollar toll but pays downwards debt faster and offers greater budgetary stability.

- See Fitch Ratings, "Fitch Ratings: Connecticut Teacher Pension Changes Plush, but Lower Fiscal Risks," news release, Feb. 28, 2019, https://www.fitchratings.com/site/pr/10064878.

- CalPERS' funding risk mitigation policy is described here: https://world wide web.calpers.ca.gov/docs/funding-risk-mitigation-policy.pdf.

- The Wisconsin Retirement System's assumed rate was decreased to 7 per centum as of 2018 and will affect required state and worker contributions kickoff in 2020.

- Wisconsin bases its post-retirement annuity benefit increases or decreases on the programme'southward investment functioning. At retirement, funds from a participant's account and the employer reserve account that are sufficient to pay an annuity for the retiree's projected lifetime are transferred to the annuity reserve account. Almanac interest is credited to this account; when the funds in the annuity reserve exceed the amount needed to pay for the existing benefit, an annuity increase is granted automatically. When funds are insufficient, the annuity payment is decreased to make up for the shortfall. More details are available at: https://etf.wi.gov/retirement/planning-retirement/annuity-payments-and-adjustments.

- The present value of liabilities—and therefore the actuarially adamant contribution rate—is lower when calculated using a discount rate of 7 pct than when calculating using the lower chance-complimentary rate (typically the return on a 30-yr Treasury pecker, currently less than 2.v percent).

- See Institutional Limited Partners Association, "Template Endorsers," https://ilpa.org/reporting-template/template-endorsers/.

- Public Pension Management and Asset Investment Review Commission, "Terminal Report and Recommendations" (2018), https://patreasury.gov/pdf/2018-PPMAIRC-Final.pdf.

- Congressional Budget Function, "The Budget and Economic Outlook: 2019 to 2029" (2019), https://www.cbo.gov/publication/54918.

- Additional contributors to lower-than-historical labor force participation include a slowdown in immigration, other demographic shifts, and depression rates of employment among people with less than a higher degree.

- Federal Reserve Bank of Cleveland, "Aggrandizement Expectations," last modified Sept. 12, 2019, https://world wide web.clevelandfed.org/our-research/indicators-and-data/inflation-expectations.aspx.

- Even if bonds yields increased significantly, this would lower the value of current bail holdings in pension funds. In a rising interest rate environment, plans would endure losses if they needed to sell bonds they purchased when yields were lower.

- Wilshire Trust Universe Comparing Service and Wilshire TUCS are service marks of Wilshire Associates Inc. ("Wilshire") and have been licensed for use past The Pew Charitable Trusts. All content of Wilshire TUCS is copyright 2019 Wilshire Associates Inc., all rights reserved.

Additional RESOURCES

More than FROM PEW

bainbridgeyeand1988.blogspot.com

Source: https://www.pewtrusts.org/research-and-analysis/issue-briefs/2019/12/state-pension-funds-reduce-assumed-rates-of-return

0 Response to "Pa Public Pensions Mamagemant and Asset Review Commission"

Post a Comment